Is AI a Bubble? What the 2026 Capex-to-Sales Ratio Actually Shows

TL;DR — The five biggest US hyperscalers will spend $660–690 billion on AI infrastructure in 2026 — nearly double 2025 — pushing their capex-to-sales ratio to roughly 34%, already above the 32% peak hit at the height of the dot-com bubble in 2000. Bulls point to real, fast-growing revenue at OpenAI and Anthropic; bears point to hyperscalers funding up to half that spending with debt and lending to the same companies that then rent the compute back. Neither side has settled it yet — here's the actual math behind both arguments.

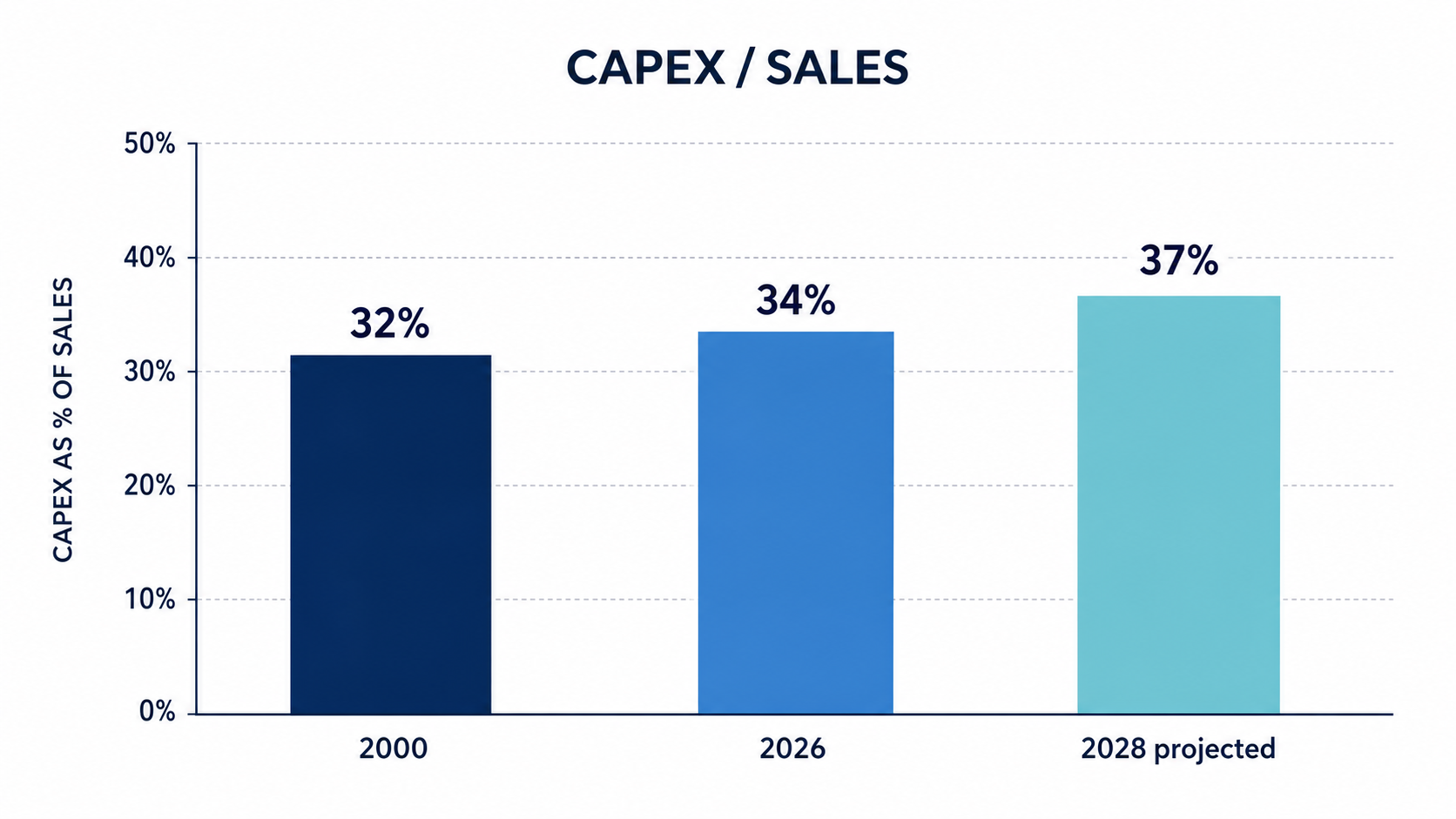

The Number Everyone's Citing: Capex-to-Sales

The single stat driving the bubble debate is how much of revenue is being plowed back into infrastructure. Morgan Stanley analyst Todd Castagno's comparison is the one making the rounds: the dot-com peak in 2000 saw a capex-to-sales ratio of 32%; the 2026 AI buildout is projected to reach 34% this year and 37% by 2028.¹ For context, the SaaS-era historical norm ran 11–16%.¹ Some individual hyperscalers are spending even more aggressively — 45% to 57% of revenue on capex, levels Morgan Stanley calls "historically unthinkable."¹

| Metric | Dot-com peak (2000) | AI buildout (2026) |

|---|---|---|

| Capex-to-sales ratio | 32% | 34% (37% by 2028E) |

| Typical prior-era norm | — | 11–16% (SaaS era) |

| Some hyperscalers individually | — | 45–57% |

## The Bull Case: Revenue Is Real and Growing Fast

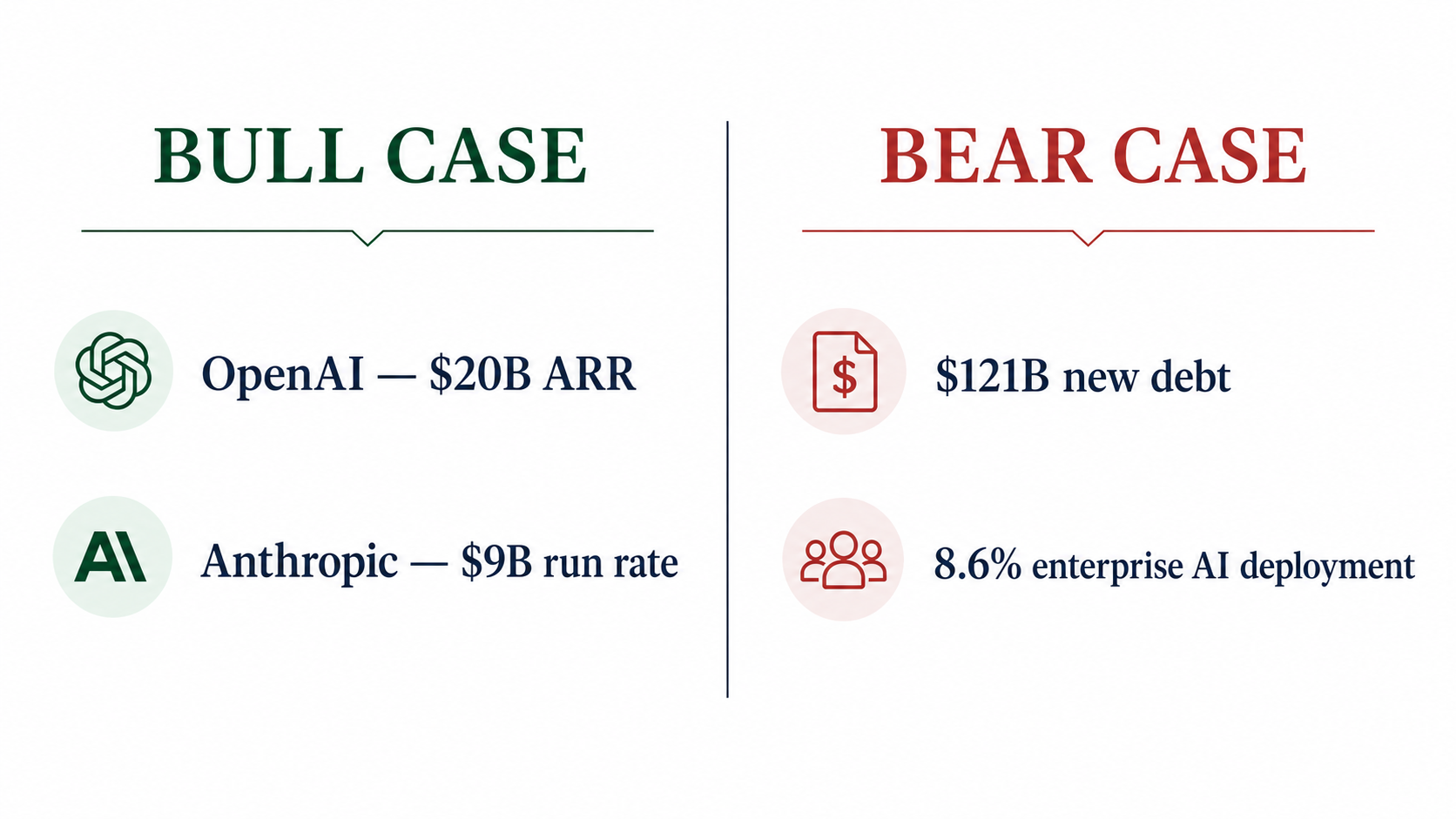

Optimists aren't just hand-waving — the underlying revenue growth is genuinely steep. OpenAI closed 2025 at roughly $20 billion in annual recurring revenue, a threefold jump from the year before, and Anthropic's revenue run rate crossed $9 billion in January 2026, up from about $1 billion at the end of 2024.² Amazon says AWS hit a $142 billion annualized run rate, with growth accelerating to 24% year-over-year — a three-year high — and its CEO has argued AI capacity is being monetized as fast as it's installed.² Fed Chair Jerome Powell has explicitly pushed back on dot-com comparisons, noting AI companies generate real revenue and that data center spending is contributing to broader GDP growth.²

The Bear Case: Debt, Circularity, and Thin Enterprise Adoption

Skeptics focus on how the spending is financed and who's actually using the output. Goldman Sachs found hyperscalers took on $121 billion in debt over the past year — a more than 300% increase from their typical debt load — and Morgan Stanley estimates Big Tech will spend about $3 trillion on AI infrastructure through 2028, with internal cash flow covering only about half.¹ Analyst Gil Luria's warning: if AI demand growth merely steadies rather than keeps accelerating, capacity will already be over-built, "the debt will be worthless, and the financial institutions will lose money."¹

The circularity concern compounds this: Microsoft invests in OpenAI, OpenAI rents Azure compute, that spending shows up as Microsoft revenue, which funds more Azure capex.¹ Critics call this a "capex echo chamber" rather than evidence of external demand.¹

Meanwhile enterprise adoption — the thing that's supposed to eventually justify all this compute — is lagging the hype. While 92% of Fortune 500 companies use ChatGPT in some capacity, only 8.6% of enterprises report AI agents actually deployed in production, and nearly two-thirds have no formal AI initiative at all.¹ A National Bureau of Economic Research study found 90% of firms report no measurable AI impact on productivity yet, even as executives project future gains.¹

## Why This Isn't Just a Tech Story

This debate already moved markets once. On June 23, 2026, Korea's KOSPI plunged hard enough to trigger a trading halt, Samsung and SK Hynix each lost 12% in a single morning, and the Nasdaq sank 2.2% that afternoon — a selloff that went global by June 24–25 as investors rotated out of AI-linked tech stocks.³ That's the same shock we covered as it happened in our piece on the no-catalyst AI selloff that hit Korea hardest and in the original AI-trade-cracked selloff a few days earlier. The market has since bounced back to a Dow 52,000 record — which is itself part of the bubble argument: sentiment is swinging on narrative, not on new productivity data.

What Would Actually Resolve This Debate

Analysts have proposed specific indicators rather than vibes. Signs the bubble is bursting: hyperscaler capex decelerating more than 20% year-over-year, enterprise AI production deployment stalling below 15%, or Nvidia's revenue concentration from its top four customers exceeding 70%.¹ Signs the floor is solid instead: healthcare and manufacturing AI spending exceeding $20 billion annually, enterprise deal conversion sustaining above 45%, or Fortune 2000 AI budgets growing 30%+ alongside documented productivity gains.¹

The most balanced read among analysts isn't binary. As one 2026 analysis put it: the companies are real, the profits are real, the technology works — the open question is whether the customers become real at the scale needed to justify $1.6 trillion in annual capex by 2031.¹²

Frequently Asked Questions

Is the AI boom definitely a bubble like the dot-com crash? Not definitively — the comparison is about spending intensity, not certainty of collapse. Capex-to-sales ratios are now above dot-com-peak levels, but unlike most dot-com-era companies, OpenAI and Anthropic have real, fast-growing revenue rather than no revenue at all.

How much are tech companies actually spending on AI in 2026? The five largest US hyperscalers (Microsoft, Alphabet, Amazon, Meta, Oracle) have committed a combined $660–690 billion in 2026 capex, nearly double 2025 levels, with Goldman Sachs projecting this could reach $1.6 trillion annually by 2031.

What's the "circular financing" concern about? It's the worry that revenue is circulating within a closed loop rather than reflecting outside demand — e.g., Microsoft funds OpenAI, which spends that money renting Microsoft's own cloud compute, which then counts as new Microsoft revenue.

Why does enterprise adoption matter so much to this debate? Because infrastructure spending only pays off if businesses actually deploy and pay for AI at scale. Right now only 8.6% of enterprises report AI agents in production, which is the gap bears point to as evidence the revenue case is still mostly promise rather than delivery.

What specific numbers would prove the bubble is bursting or not? A deceleration in hyperscaler capex growth of more than 20% year-over-year, or Nvidia's top four customers exceeding 70% of its revenue, would support the bubble-bursting case. Sustained 30%+ AI budget growth at large enterprises with documented productivity gains would support the opposite.

Key Takeaways

- The 2026 AI capex-to-sales ratio (34%, projected 37% by 2028) has already surpassed the 32% peak from the dot-com bubble in 2000.

- Unlike most dot-com companies, OpenAI ($20B ARR) and Anthropic ($9B run rate) have real, fast-growing revenue — the bull case isn't imaginary.

- Hyperscalers have taken on $121 billion in new debt (up 300%) to help fund an estimated $3 trillion infrastructure buildout through 2028, with cash flow covering only about half.

- Only 8.6% of enterprises report AI agents deployed in production, which is the core gap between infrastructure spending and proven business demand.

- The June 23, 2026 Korea-led global selloff shows this debate isn't academic — it already moves markets, and the subsequent recovery to Dow 52,000 shows how sentiment-driven the swings are.

Sources 1. Futurum Group: AI Capex 2026: The $690B Infrastructure Sprint 2. Yahoo Finance: AI spending is surging, but a hidden risk is getting overlooked 3. Carus Signal: The AI Sell-Off With No Catalyst — and Why Korea Fell Hardest

Tags: #AI #AIBubble #Markets #BigTech #Investing #Explainer

Comments ()