Why Memory Chip Stocks Crashed 14% During a Shortage — and What a 6x P/E Really Means

TL;DR — On July 2, 2026, SK Hynix fell about 14.6% and Samsung about 9% in a single session — hard enough to trigger an emergency halt on Korea's Kospi — while the underlying product, AI memory, is so scarce that Micron's quarterly revenue just quadrupled to $41.5 billion. That contradiction isn't a mistake. Memory stocks trade at single-digit P/E ratios (Micron ~9.6x, SK Hynix ~6x forward) precisely because the market is already pricing the cycle turning, and history says the stock peaks roughly two quarters before the fundamentals do. Here's the cycle math that explains why a shortage and a sell-off can happen the same week.

The Paradox: Record Fundamentals, Falling Stocks

The setup looks self-contradictory on the surface:

| Signal | What's happening | Direction |

|---|---|---|

| Micron fiscal Q3 2026 revenue | $41.5B, ~4x year-ago | 🚀 Up |

| Micron Q3 gross margin guidance | ~81% | 🚀 Up |

| DRAM contract prices (Q1 2026) | +90% quarter-on-quarter | 🚀 Up |

| NAND contract prices (Q1 2026) | +50% quarter-on-quarter | 🚀 Up |

| Supply outlook | Sold out through 2026, into 2027 | 🔒 Tight |

| SK Hynix stock, July 2 | −14.6% intraday | 📉 Down |

| Samsung stock, July 2 | −9% intraday | 📉 Down |

So the world can't make enough of the product, prices are up double-digit-percent per quarter, margins are at record highs — and the stocks just had one of their worst days of the year. Both SK Hynix and Micron crossed the $1 trillion valuation mark earlier in 2026 on exactly this AI-memory story. If demand is the whole thesis, the sell-off makes no sense.

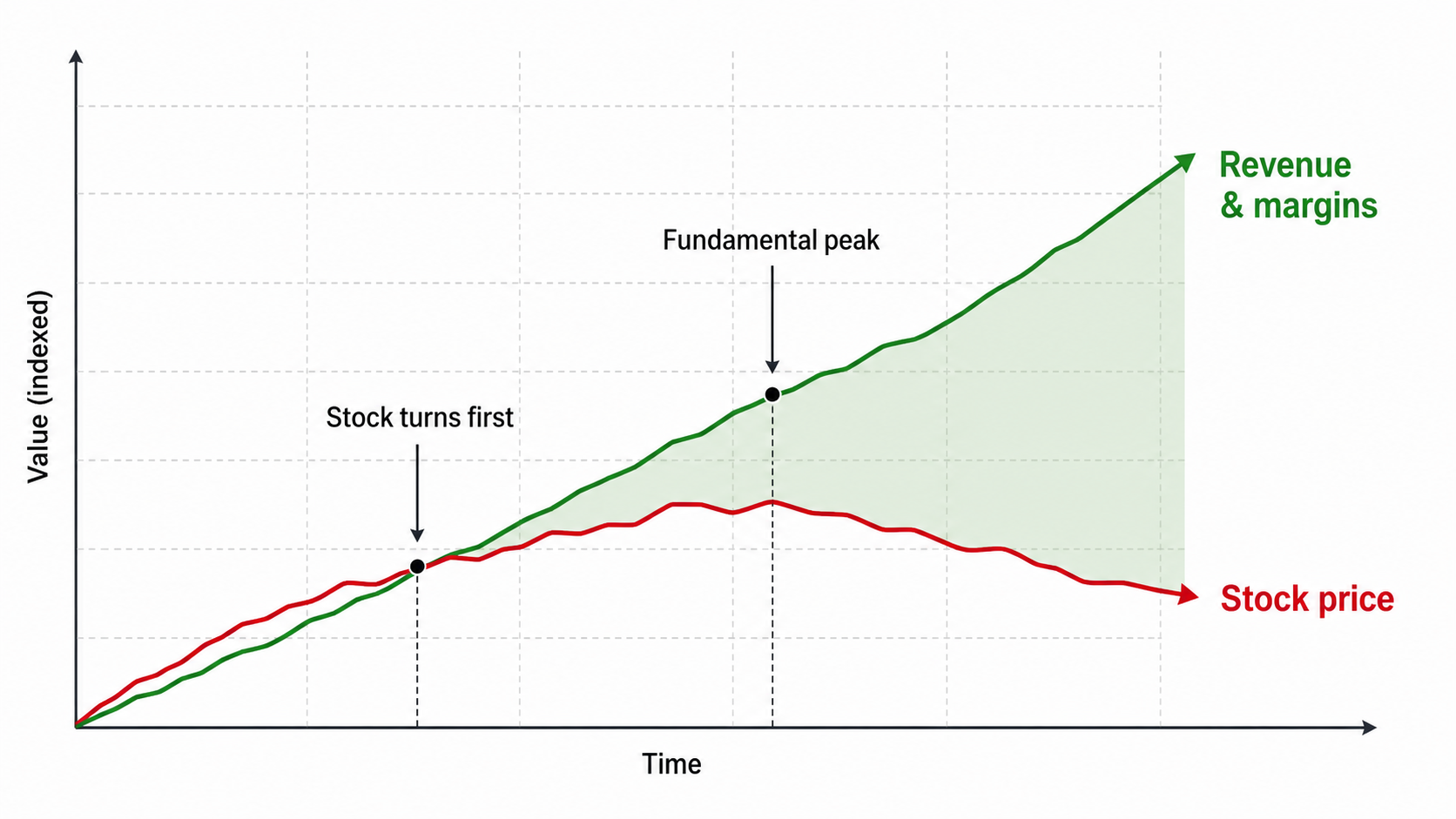

The resolution is that stock prices don't track today's earnings. They track the market's guess about the next turn in earnings. And for memory, that turn is the entire game.

## The Core Reason: Memory Is the Most Cyclical Business in Tech

DRAM and NAND are commodities made by essentially three companies — Samsung, SK Hynix, and Micron — that together produce nearly all of the world's supply. Commodities with concentrated supply run in violent boom-and-bust cycles:

- Shortage → prices spike → margins explode → all three pour capex into new capacity.

- That new capacity lands 18–24 months later, usually after demand has cooled.

- Glut → prices collapse → margins go negative → capex freezes.

- Supply tightens again → back to step 1.

The critical trading insight: the stock leads the fundamentals by about two quarters. In the last big cycle, Micron's stock peaked around $64 in May 2018, but revenue and margins didn't actually top out until Q4 2018 — the share price called the top roughly two quarters early. Traders who waited for the earnings peak to sell were already down badly by the time it arrived.

That's why a single day of AI-capex jitters — a hint that hyperscaler spending might plateau, a rumor of new fab capacity — can knock 14% off a memory stock even while it's shipping record revenue. The market isn't reacting to this quarter. It's voting on whether this is the two-quarters-early top.

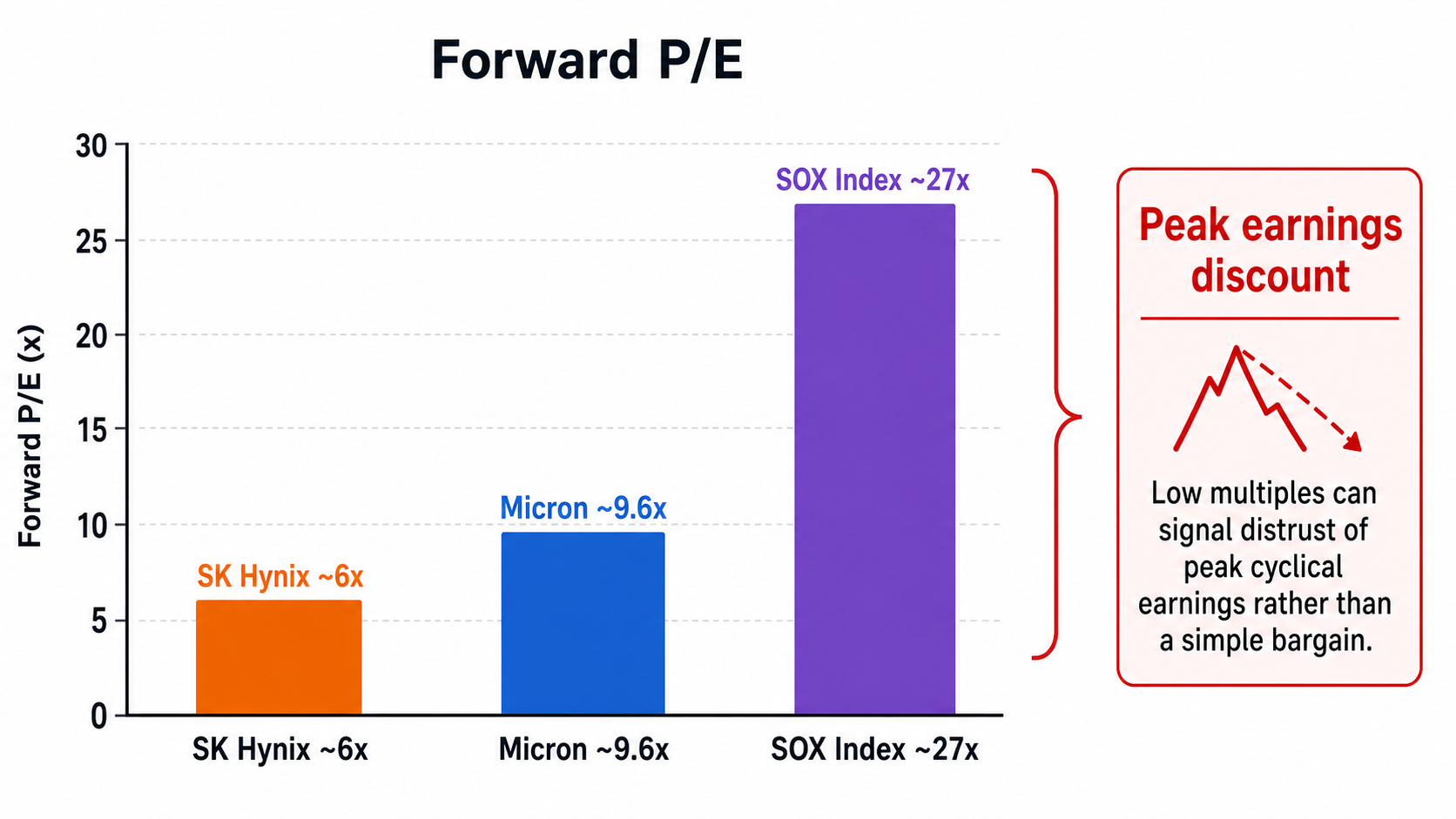

What a 6x P/E Is Actually Telling You

Here's the number that reframes everything. After a rally that took both companies past $1 trillion, the memory names trade at strikingly low multiples:

| Company | ~Forward P/E | 2026 YTD stock move* |

|---|---|---|

| SK Hynix | ~6x | +186% |

| Micron | ~9.6x | +141% |

| SanDisk | — | +156% |

| Samsung | — | +114% |

| Philadelphia Semiconductor Index (SOX) | ~27x | — |

*YTD figures as reported in late-spring 2026; they move with the market.

A ~6x forward P/E on a company whose order book is sold out into 2027 looks absurdly cheap next to the 27x that the broad chip index carries. But it isn't a bargain the market missed — it's the market refusing to capitalize peak earnings. A P/E is price divided by expected earnings. When investors assign 6x, they're implicitly saying: we don't believe next year's earnings will look like this year's; we think they'll fall, so we won't pay a normal multiple for them.

Do the reverse math. If the market thought Micron's ~$41B-a-quarter run rate were durable and deserved even a market-average 18x, the stock would be worth roughly triple. It isn't priced that way because everyone remembers step 3 of the cycle. The low multiple is the bearish forecast, hiding in plain sight inside a bullish tape.

## How to Actually Read a Memory Stock

For anyone weighing these names, the useful questions aren't "is there a shortage?" (yes) or "are earnings good?" (spectacular). They're:

- Where are we in the cycle? Some analysts argue the 2026 rally has only entered its "middle phase," with the real earnings peak landing somewhere between Q4 2026 and Q2 2027. If true, the stock top could arrive before that — potentially in the back half of 2026.

- What's capex doing across all three? Rising fab investment is the seed of the next glut. The shortage feels permanent right up until the new supply switches on.

- Is AI demand a step-change or a spike? The entire bull case rests on HBM and AI-server memory being structurally different from PC/phone DRAM. If it's structural, the cycle is milder. If it's just a bigger spike, the bust is bigger too.

The single-digit P/E is the tell: the market has already placed its bet that this is a spike, not a plateau. You're not being offered cheap durable earnings — you're being offered a wager on cycle timing.

Frequently Asked Questions

How can memory stocks fall while there's a chip shortage? Because share prices reflect expectations about future earnings, not current ones. Memory is deeply cyclical, and the stock historically peaks about two quarters before revenue and margins do. A shortage today tells you nothing about whether the market thinks the cycle is about to turn — and it's the turn that moves the stock.

Why do Micron and SK Hynix trade at such low P/E ratios? A single-digit forward P/E on a highly cyclical business is the market's way of saying it won't pay a full multiple for earnings it expects to decline. It's not necessarily "cheap" — it's earnings the market distrusts. Low-P/E memory stocks at a cycle peak have historically been value traps, not bargains.

Did the July 2, 2026 sell-off mean the AI trade is over? Not by itself. It was driven by an overnight slump in US chip stocks spreading to Asia, amplified by memory's inherent volatility and stretched positioning after a huge year-to-date run. One violent session in a cyclical group is normal; it's a warning about timing risk, not a verdict on AI demand.

Is Micron or SK Hynix the "better" memory stock? They're highly correlated because they sell the same commodities into the same cycle. SK Hynix has led on HBM for AI and carried an even lower multiple; Micron gives US investors direct exposure and just posted a ~$41.5B quarter. The bigger decision isn't which one — it's whether you want cyclical memory exposure at all, and at what point in the cycle.

What historically ends a memory upcycle? New supply. High prices pull massive capex into new fabs from all three makers; that capacity lands 18–24 months later, often just as demand cools, flipping shortage into glut and crushing prices and margins. The AI bull case is that demand is structural enough to break this pattern — an unproven claim.

Key Takeaways

- Memory stocks can crash during a shortage because prices discount the next turn in a notoriously cyclical business, not today's record fundamentals.

- Historically the stock peaks ~2 quarters before earnings do — Micron's 2018 stock top preceded its fundamental peak by about two quarters.

- The single-digit forward P/E (SK Hynix ~6x, Micron ~9.6x) vs. the SOX index's ~27x isn't a bargain — it's the market pricing in an expected earnings decline.

- Micron's fiscal Q3 2026 was genuinely historic (~$41.5B revenue, ~4x YoY, ~81% margin guidance), and supply is sold out into 2027 — yet none of that resolves the timing question.

- For memory, the real question is never "is there demand?" but "where are we in the cycle, and is AI demand structural or just a bigger spike?"

Sources 1. CNBC: Samsung, SK Hynix shares tumble over 9% as chip rout spreads from Wall Street 2. Stocks Down Under: Micron's Rivals Just Crashed 14%: What SK Hynix and Samsung's Slide Means for the Memory Trade 3. CNBC: Micron (MU) Q3 2026 earnings report — revenue quadruples on memory crunch 4. TradingKey: SK Hynix vs. Micron: Which Memory Chip Is the Better Investment? 5. Euronews: Memory chip giants SK Hynix and Micron cross $1tn valuation amid AI mania 6. CNBC: Beware the boom and bust cycle of memory stocks, investors warn amid AI excitement

Tags: #Semiconductors #MemoryChips #Micron #SKHynix #Investing #Explainer

Comments ()