Should Stablecoins Pay Yield? The $1.5 Trillion Question Splitting Banks and Crypto

TL;DR — The single biggest thing blocking the US Digital Asset Market Clarity Act (CLARITY Act) in the Senate is a narrow-sounding question with huge stakes: should stablecoins be allowed to pay yield? Three competing studies reach wildly different conclusions — a White House model says banning yield barely moves bank lending (0.02%), while bank-funded modeling projects up to $1.5 trillion in lost lending capacity if yield-bearing stablecoins compete freely with deposits. Here's what each side is actually measuring, and why they disagree so much.

What's Actually Being Debated

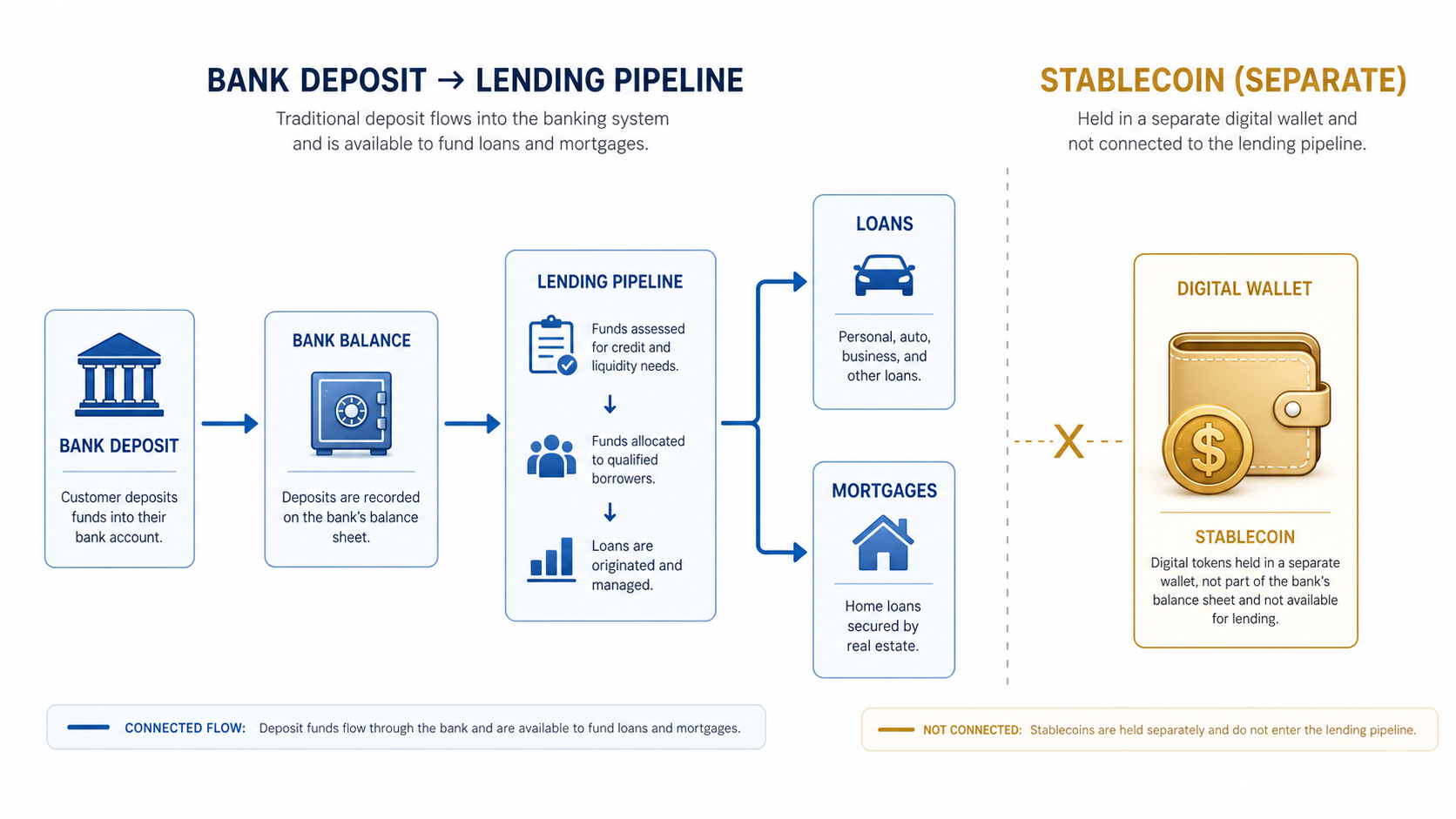

Stablecoins are cryptocurrencies pegged to a stable asset (usually the US dollar), designed to work as digital cash rather than a speculative bet. The CLARITY Act would create a federal framework for them — but it's stalled in the Senate Banking Committee with no scheduled markup, entirely because of one unresolved question: can a stablecoin issuer pay you interest for holding it, the way a savings account does?¹

The concern is straightforward once you see it: a non-yield-bearing stablecoin is just a payment tool, similar to holding cash. A yield-bearing one starts to look and act like a bank deposit — except issued by a company that isn't a bank and doesn't have the same reserve requirements or deposit insurance. Once stablecoins can compete on yield, banking groups argue they stop being payment rails and start pulling deposits directly out of the banking system.²

## Three Studies, Three Very Different Numbers

This is the part that makes the debate genuinely hard to referee — credible-looking research lands in very different places depending on who funded it and what they modeled:

| Study | Source | Key finding |

|---|---|---|

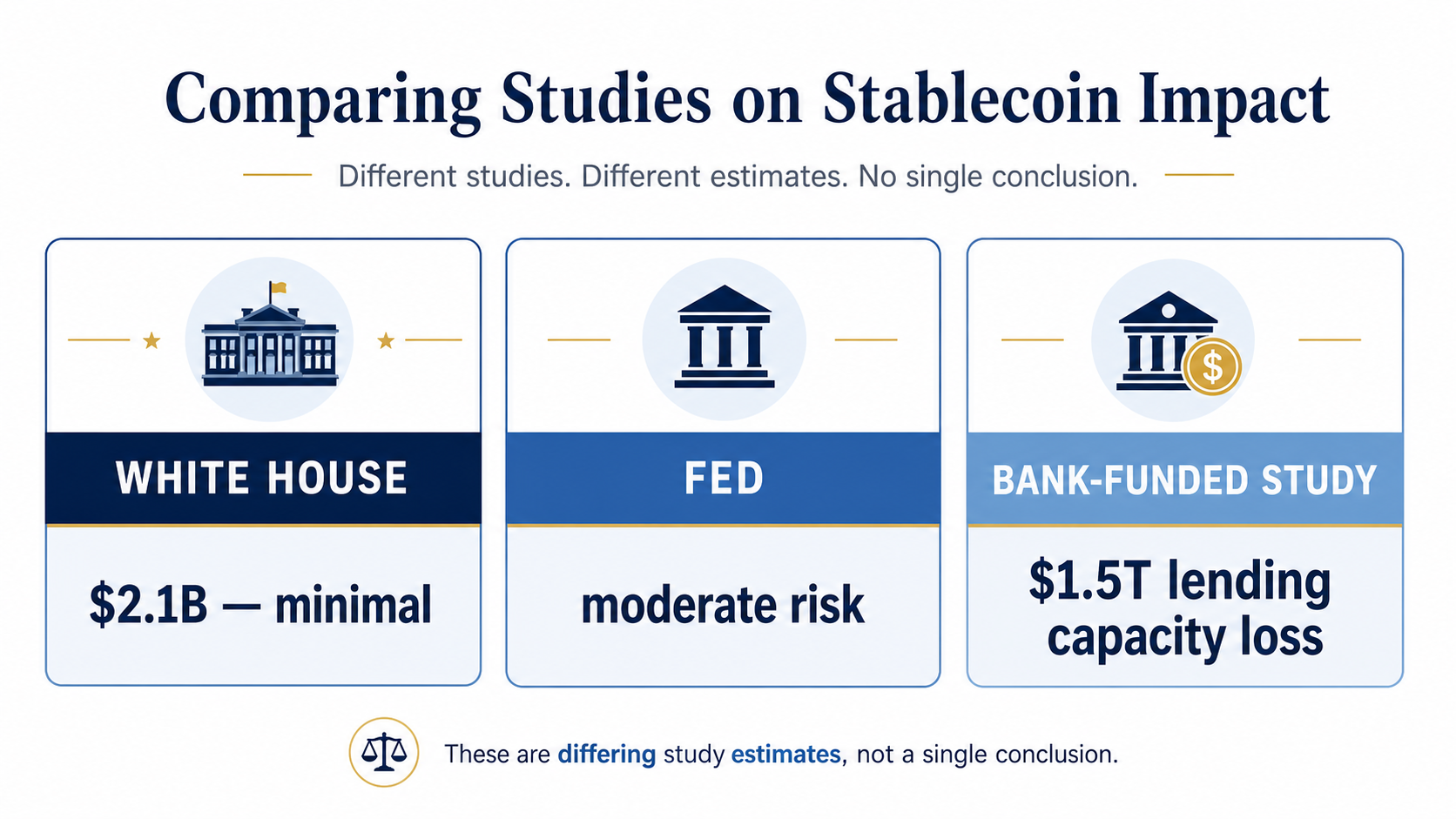

| White House CEA (Apr 8, 2026) | Council of Economic Advisers | Banning stablecoin yield boosts bank lending by just $2.1B (0.02%); community banks gain only $500M³ |

| NY Fed staff report | Federal Reserve Bank of New York | Identifies a disintermediation channel: partner banks see ~67% higher interbank payments and more reserve volatility as deposits shift to stablecoins³ |

| Industry/bank-funded model | Banking sector groups | Without yield: deposits fall ~6.2%, ~$250B lending capacity lost. With yield-competitive stablecoins: deposit losses jump to ~25.9%, lending capacity falls by ~$1.5 trillion, hitting community/small banks hardest³ |

The gap between "$2.1 billion, doesn't matter" (White House) and "$1.5 trillion, hits small banks hardest" (bank-funded model) is enormous — and it comes down to a modeling assumption: how much of existing bank deposits would actually move into stablecoins if they paid competitive yield. The CEA model assumes very little switching; the bank-funded model assumes stablecoins become close substitutes for savings deposits once yield is allowed.³

## Is the Threat Even Big Enough to Matter Yet?

Here's a genuinely important counterpoint that gets less attention: stablecoin market capitalization was only around $315 billion as of early April 2026 — dwarfed by roughly $8 trillion in US bank deposits.¹ At that scale, even aggressive growth would take years to meaningfully dent the deposit base the bank-funded model worries about. A BIS speech specifically noted this gap, cautioning against assuming stablecoins will be as transformative as the hype suggests, at least on the current growth trajectory.¹

There's also a regulatory wrinkle complicating the picture further: the fastest-growing stablecoin, Tether's USDT, doesn't comply with the stablecoin laws of major jurisdictions — meaning even if the CLARITY Act resolves the yield question for compliant US issuers, the largest player in the market may not be playing by the new rules anyway.¹

Why This Isn't Just a Crypto Story

Stablecoins already show measurable effects beyond crypto trading. A Bank for International Settlements working paper found a $3.5 billion stablecoin inflow lowers 3-month Treasury bill yields by 0.71 basis points on impact, and up to 4 basis points within 10 days — with the effect growing larger during periods of Treasury market stress.⁴ Treasury Secretary Bessent and a Fed governor have argued stablecoins could eventually generate trillions in new Treasury demand, since issuers typically back their coins with short-term Treasury holdings.⁴ That's a genuinely different economic story from "crypto speculation" — it's stablecoins acting as a new, fast-growing buyer of US government debt.

Frequently Asked Questions

What is the CLARITY Act and why is it stalled? The Digital Asset Market Clarity Act would create a federal regulatory framework for stablecoins and other digital assets in the US. It has no scheduled Senate Banking Committee markup because lawmakers haven't resolved whether stablecoins should be legally allowed to pay yield to holders.

Why does paying yield on stablecoins worry banks? A stablecoin that doesn't pay yield functions like digital cash. One that does pay yield starts competing directly with savings accounts and CDs, potentially pulling deposits out of the banking system — deposits that banks currently use to fund loans and mortgages.

How big is the stablecoin market compared to the banking system right now? Stablecoins totaled about $315 billion in market cap as of early April 2026, compared to roughly $8 trillion in US bank deposits — meaning the current scale is still small relative to the risk being debated, even if the growth rate is fast.

Do stablecoins actually affect US Treasury markets? Yes, measurably. A BIS study found a $3.5 billion stablecoin inflow lowers 3-month Treasury bill yields by up to 4 basis points within 10 days, since most stablecoin issuers hold short-term Treasuries as reserves backing their coins.

Why do the CEA, Fed, and bank-funded studies disagree so much? They use different assumptions about how many depositors would actually move their money into yield-bearing stablecoins. The White House study assumes minimal switching; the bank-funded model assumes stablecoins become close substitutes for bank deposits once they can compete on yield, producing a far larger estimated impact.

Key Takeaways

- The CLARITY Act is stalled in the Senate specifically over whether stablecoins can legally pay yield — not over stablecoins generally.

- Three credible-looking studies disagree by orders of magnitude: $2.1B (White House), moderate disintermediation risk (NY Fed), and up to $1.5 trillion in lost lending capacity (bank-funded model).

- At $315 billion, stablecoins remain small relative to the $8 trillion US deposit base — the debate is really about trajectory, not current impact.

- Tether's USDT, the largest and fastest-growing stablecoin, doesn't comply with major-jurisdiction stablecoin laws, complicating any regulatory fix.

- Stablecoins already measurably move Treasury bill yields, making this a monetary policy question as much as a crypto or banking one.

Sources 1. BIS: Stablecoins: framing the debate (Pablo Hernández de Cos speech) 2. Federal Reserve: Banks in the Age of Stablecoins: Lessons from Their Historical Responses to Financial Innovations 3. Forbes: Why Bank And Crypto Studies Disagree Sharply On Stablecoin Yield Risks 4. BIS Working Papers No. 1270: Stablecoins and safe asset prices

Tags: #Stablecoins #Crypto #CLARITYAct #Banking #Regulation #Explainer

Comments ()